Let us know who you are

Ready to Implement

VantageScore 4.0 for Mortgage?

Let's Get Started

Resource Center

Mortgage Migration Playbook

VantageScore Migration Playbook outlines how to implement VantageScore 4.0 for underwriting mortgages.

Mortgage FAQs

Frequently Asked Questions about VantageScore 4.0 for Mortgage.

Digital Analytics Tools

Lenders gain timely data insights into the predictive and inclusionary power of VantageScore via a suite of free access tools: CreditGauge™, Inclusion360®, RiskRatio™ and MarketGain™.

VantageScore 4.0 Produces Superior Mortgage Risk Differentiation Compared to FICO

OGMA Risk and Analytic Study

VantageScore 4.0 for Mortgage Pre-screening and Pre-approval

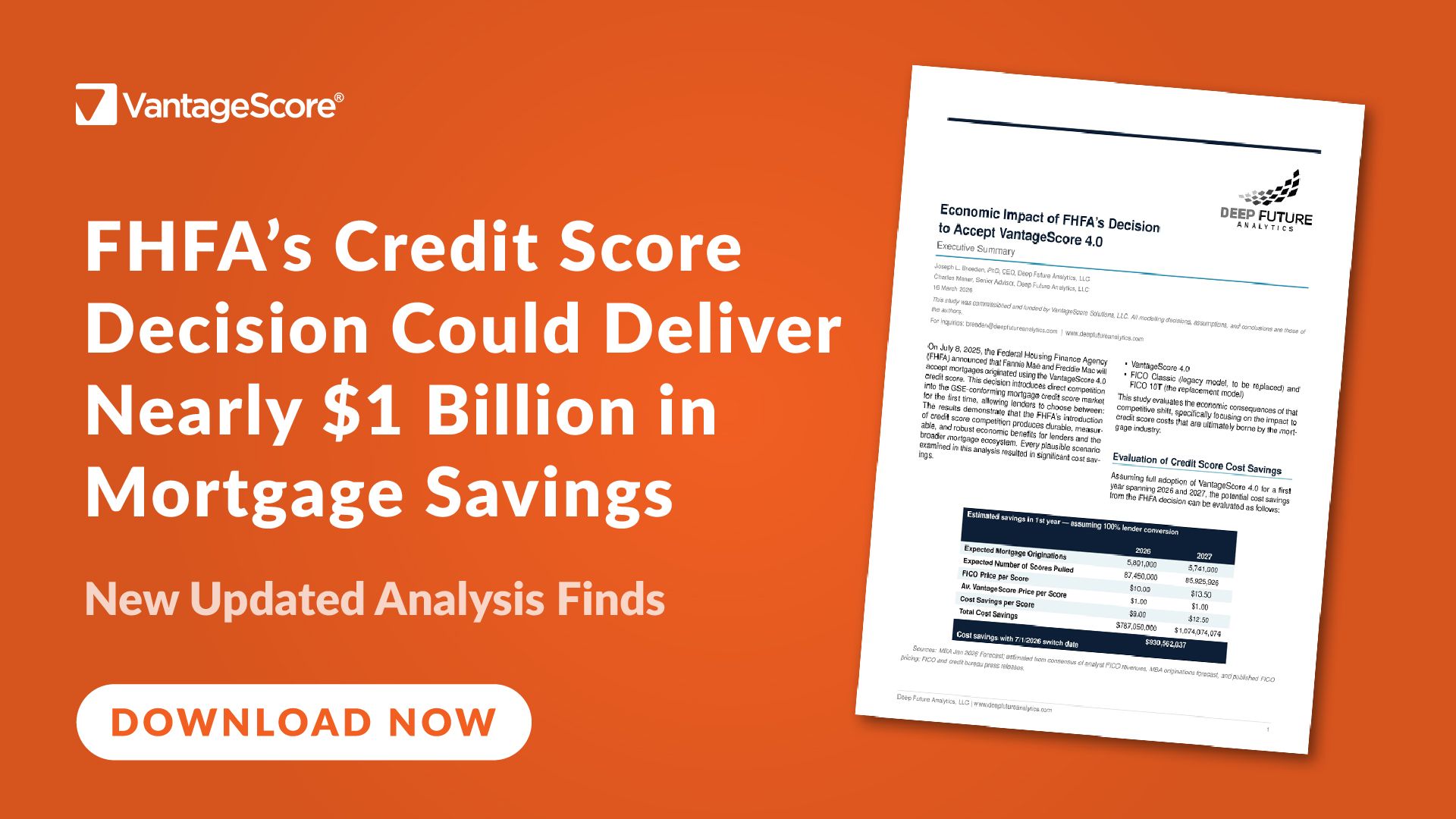

Deep Future Analytics Study

VantageScore 4.0 and Classic FICO Comparison

VantageScore Accessible Mortgage Lending

Speak With Us

External Resources

April 24, 2026

All Systems Go for VantageScore in the Mortgage Market: VantageScore CEO on Bloomberg’s ‘The Close’

July 25, 2025

VantageScore 4.0 Brings New Predictive Power and More Data to Fannie and Freddie Backed Mortgages: VantageScore® CEO on Bloomberg TV

July 18, 2025

Modernizing the Mortgage Credit Scoring System is Long Overdue, VantageScore CEO tells CNBC

Thanks to a landmark decision by the Federal Housing Finance Agency (FHFA), mortgage lenders that sell loans to either Fannie Mae or Freddie Mac (also known as the GSEs) will be required to use the VantageScore 4.0 model.

The FHFA's decision opens the door to millions more qualified applicants without lowering credit risk standards.

The result of the decision is a mortgage lending industry that serves consumers through the advancement of financial inclusion and supports mortgage lenders seeking to grow their portfolios.

What does it mean for the mortgage industry?

In 2024, several government-sponsored enterprises (GSEs) adopted VantageScore 4.0, including:

BMO Bank is a purpose-driven organization that is focused on leveling the playing field in underserved communities and creating the conditions for inclusive economic growth. VantageScore has provided us with the opportunity to provide fair and accurate credit scores to a broader population, and we look forward to leveraging VantageScore for mortgage lending in the future to help further close the housing gap.

Mark Shulman, Head of Consumer Lending, BMO Bank

We believe in driving financial inclusion and creating more equitable access to credit in the communities we serve. We've been using VantageScore 4.0 for our auto loans and credit cards and that's provided us with a new pathway to provide fair and accurate credit scores to a broader population, creating opportunities for us to lend credit safely and soundly to consumers historically left behind. We look forward to leveraging VantageScore 4.0 for mortgage lending in the future.

Richard Wada, Chief Lending Officer at Patelco Credit Union

Approximately 33 million more Americans can be scored by our models.

21% of millennials have "thin files," making it difficult for lenders to see them as strong borrowers and leading to more young consumers not able to get the credit they need.

Demographic Breakdown

Breakdown of Newly Scorable Consumers

More Potential Customers

Strong Risk Management

VantageScore is at the cutting edge of predictive power thanks in part to its highly sophisticated model architecture and its innovative use of data. The VantageScore 4.0 model features the use of trended credit data and machine learning to drive predictive performance. VantageScore provides more precise decisioning enabling more mortgage application approvals while limiting defaults.

Fannie Mae, Freddie Mac and many others have conducted independent analysis on the published data on VantageScore 4.0 and the legacy models. They all found that VantageScore 4.0 was more predictive and particularly better at identifying those who would default on their mortgages at the lower score ranges (which is where most defaults occur). The more accurate the model, the less risk of defaults.

Close The Homeownership Gap

More Consumer Friendly

More Potential Customers

Strong Risk Management

VantageScore is at the cutting edge of predictive power thanks in part to its highly sophisticated model architecture and its innovative use of data. The VantageScore 4.0 model features the use of trended credit data and machine learning to drive predictive performance. VantageScore provides more precise decisioning enabling more mortgage application approvals while limiting defaults.

Fannie Mae, Freddie Mac and many others have conducted independent analysis on the published data on VantageScore 4.0 and the legacy models. They all found that VantageScore 4.0 was more predictive and particularly better at identifying those who would default on their mortgages at the lower score ranges (which is where most defaults occur). The more accurate the model, the less risk of defaults.

Close The Homeownership Gap

More Consumer Friendly

Portfolio Management

VantageScore credit scores are effective tools for monitoring the ongoing risk of mortgage portfolios.

Mortgage Backed Security Analysis

The VantageScore model is often used in loan-level valuation analyses for previously issued residential mortgage-backed securities.