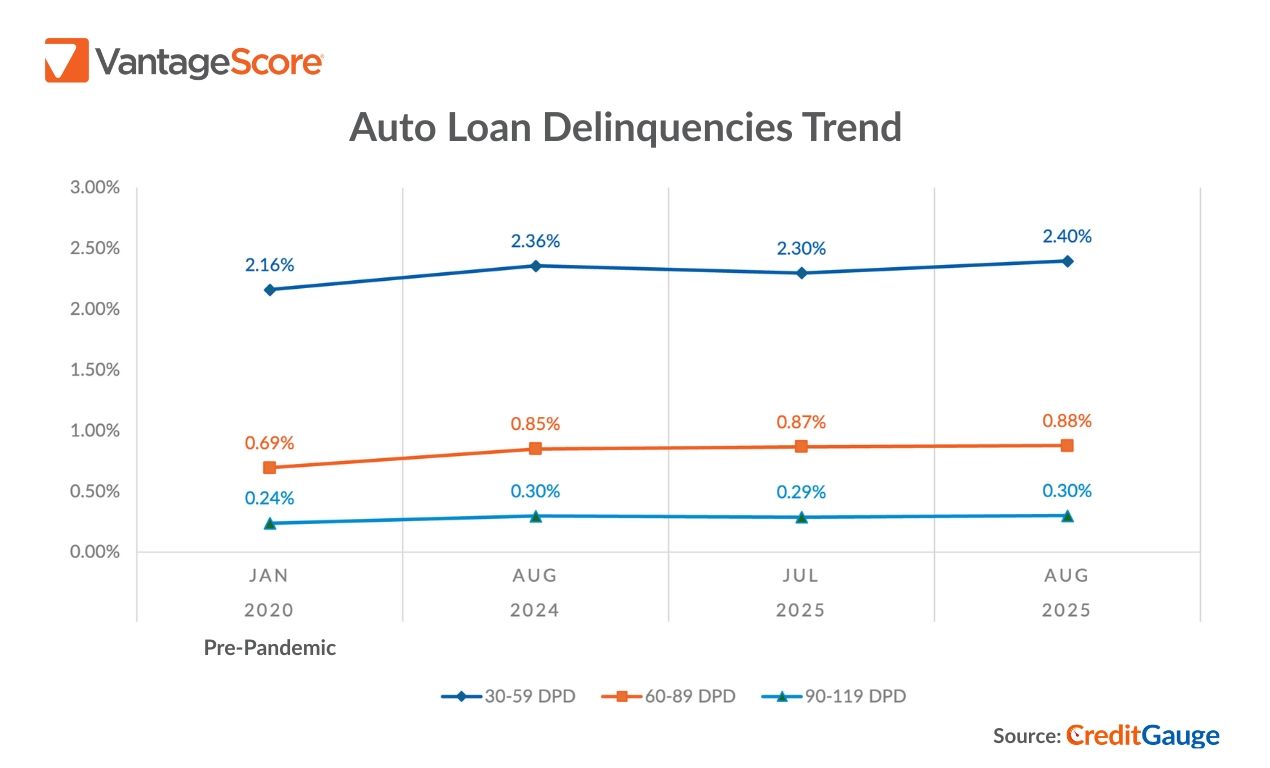

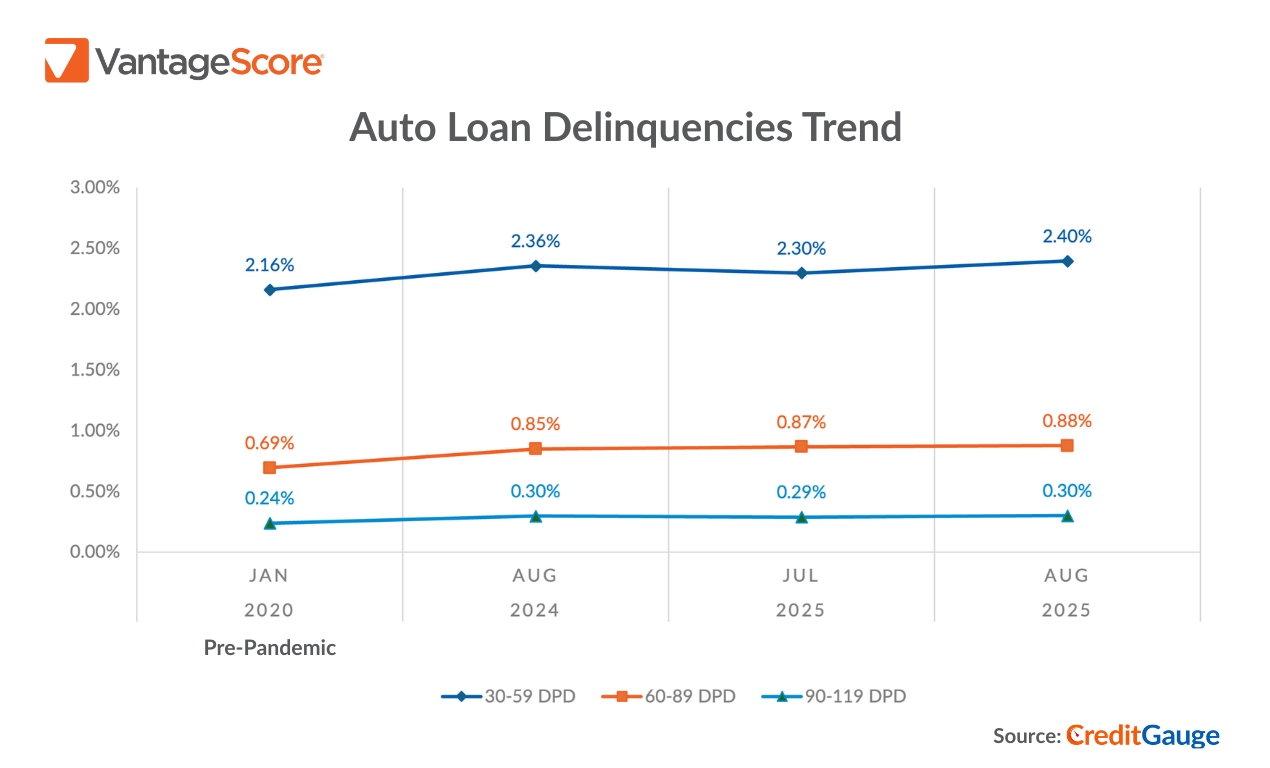

Year-over-year, credit delinquencies rose across nearly all VantageScore credit tiers and almost all delinquency categories, indicating that repayment pressures are affecting even the most creditworthy consumers. For example, Auto Loan delinquencies increased across all stages, surpassing pre-pandemic levels, according to the August 2025 edition of CreditGauge™ published today by VantageScore. The average VantageScore 4.0 credit score remained stable at 701 in August.

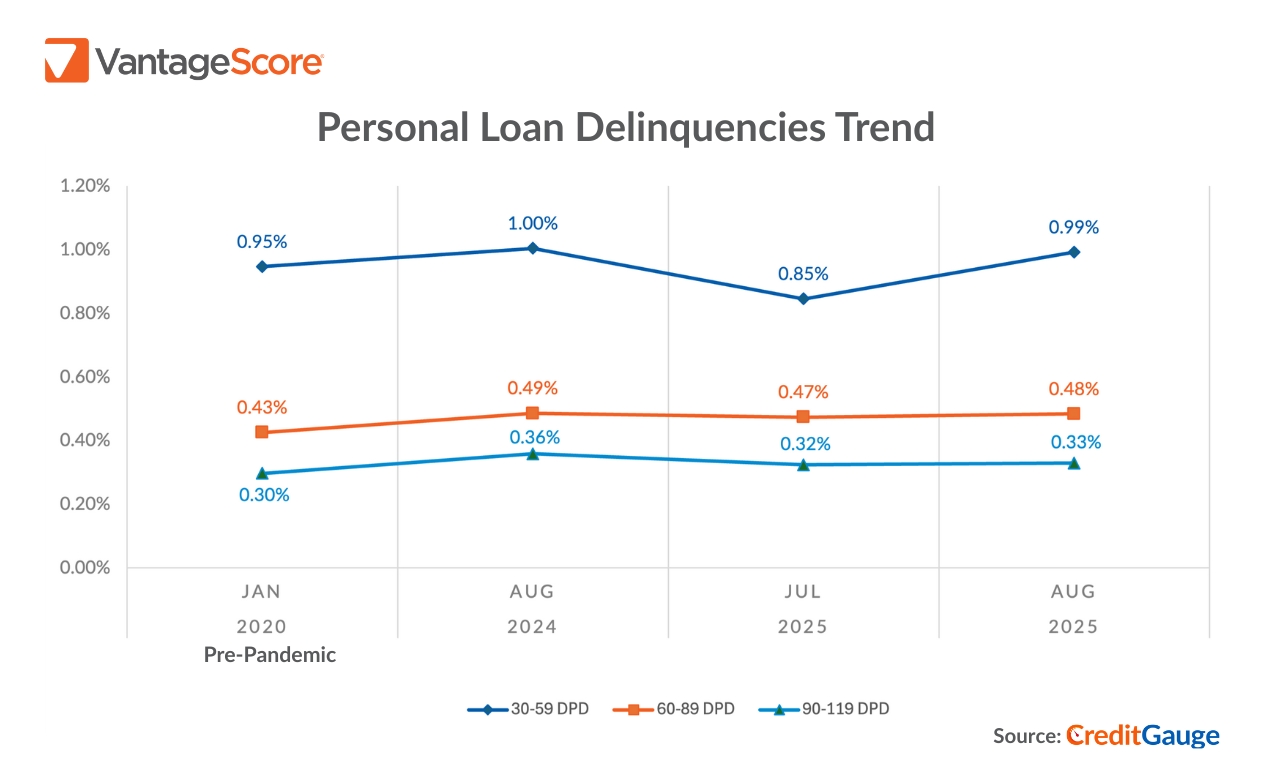

The broad-based decline in consumer credit quality indicates that economic pressures are no longer concentrated among some VantageScore credit tiers and income levels,” said Susan Fahy, EVP and Chief Digital Officer at VantageScore. “For example, the increase in Auto Loan and Personal Loan credit delinquencies likely reflects, in part, the compounding effects of sustained inflation, consistently elevated interest rates, higher borrowing costs, and an unsteady employment picture.

Watch CreditGauge LIVE for additional key insights from the August 2025 edition of CreditGauge that include:

VANTAGESCORE SUPERPRIME IMPACTED: In August 2025, credit delinquencies increased year-over-year across all VantageScore credit tiers and almost all delinquency categories. The most significant increase occurred among VantageScore Superprime borrowers (781-850) in the 90-119 Days Past Due (DPD) category, with an over 300% spike in delinquency levels. While absolute Superprime credit delinquency levels remain extremely low, this sharp uptick indicates weakened repayment behavior even among the most creditworthy consumers.

UNSECURED CREDIT ORIGINATIONS GROW AS CONSUMERS SEEK LIQUIDITY THROUGH REFINANCING: In August 2025, unsecured loan originations rose across key products on a month-over-month basis, led by Personal Loans (+0.45%) and Credit Cards (+0.39%). Unsecured credit originations rose faster than secured ones, reflecting increased demand for liquidity, as consumers refinance debt with unsecured loans.

RISING CREDIT CARD BALANCES INDICATE CONSUMER CREDIT STRESS: In August 2025, the average Credit Card balance rose to $6.5K, up $96 year-over-year and $67 from July 2025. The utilization rate also increased to 30.77%, suggesting increased consumer reliance on revolving credit amid persistent cost-of-living pressures.

CreditGauge is a monthly analysis highlighting the overall health of U.S. consumer credit. To download this month’s full CreditGauge report, visit the VantageScore website.

Follow VantageScore on LinkedIn and YouTube to watch CreditGauge LIVE, a monthly video series featuring our latest insights on consumer credit data and analysis.