- Average VantageScore Credit Score Drops to 701

- Mortgages and Auto Loans Lead Increase in Credit Delinquencies

- Secured Credit Originations Soften

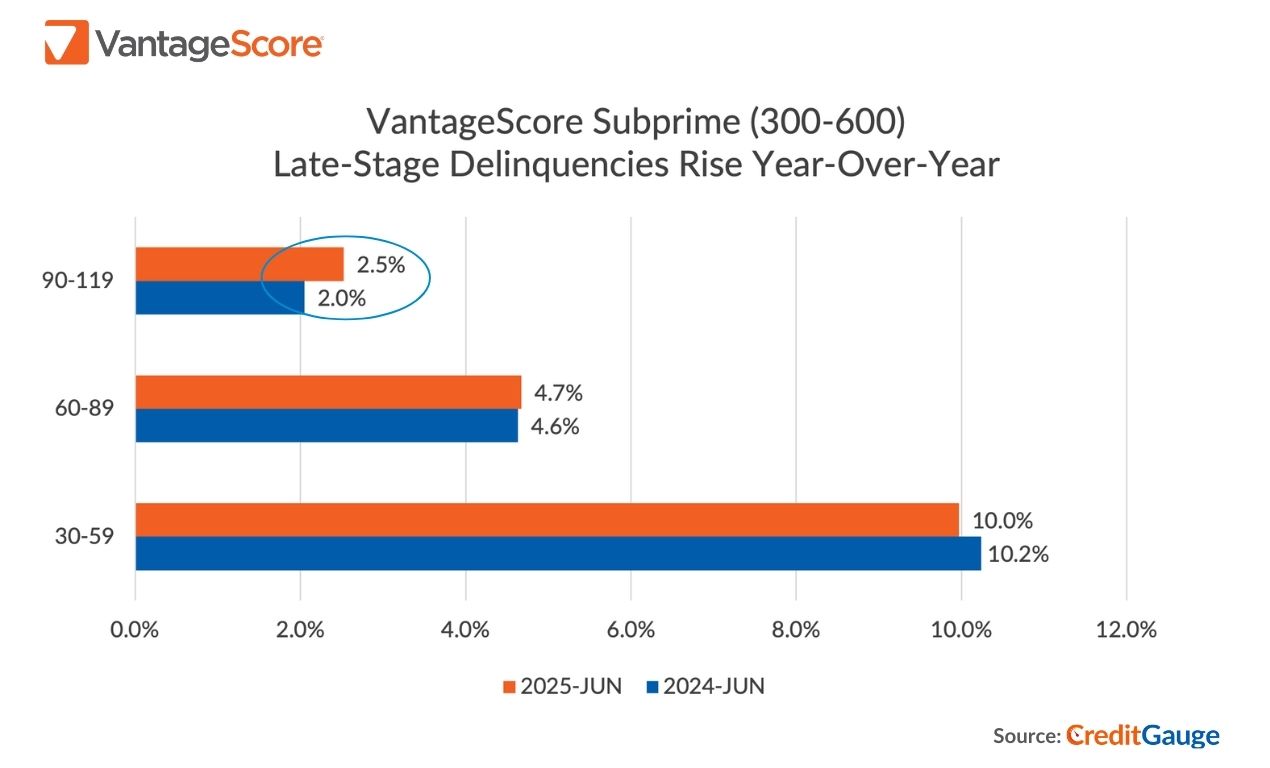

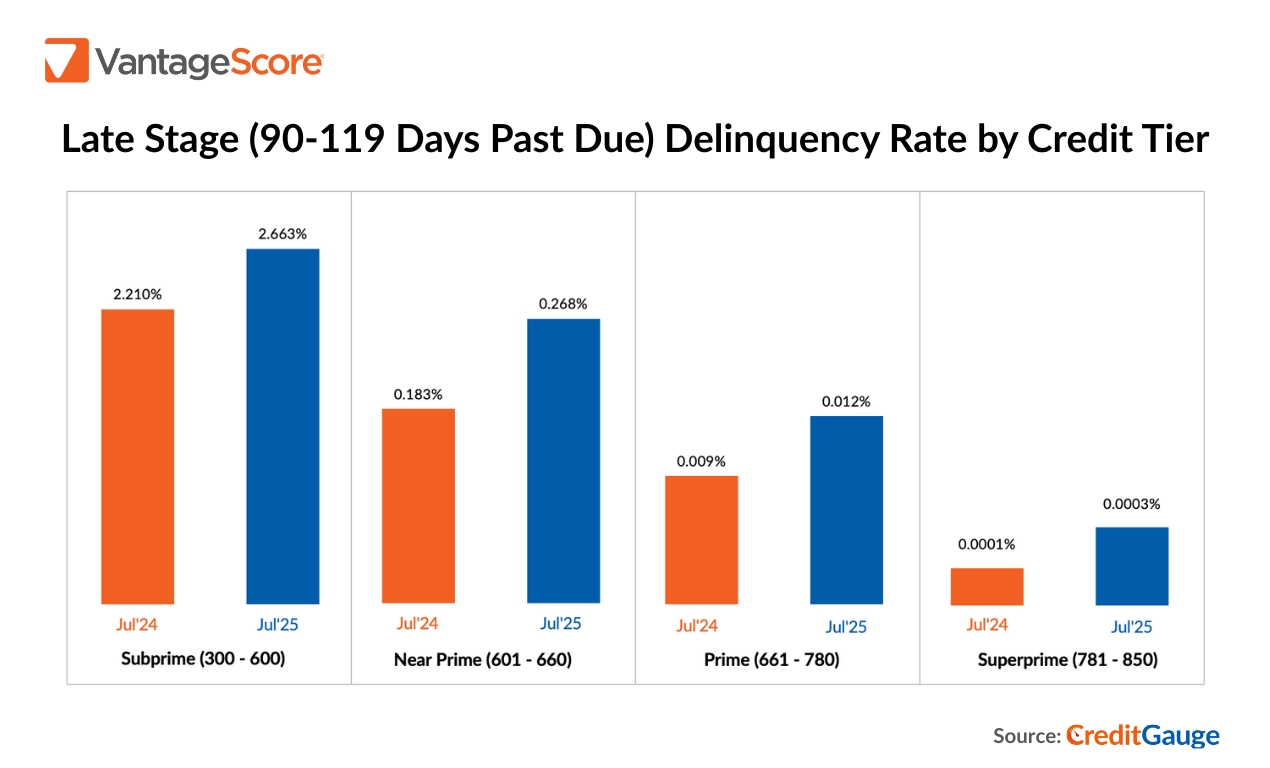

SAN FRANCISCO - August 25, 2025 Late-stage delinquencies increased across all credit tiers led by the VantageScore Superprime and VantageScore Prime segments, according to the latest edition of CreditGauge™ published today by VantageScore. Credit delinquencies over 90 days late were up 109% year-over-year in the VantageScore Superprime segment, while Prime saw a 47% increase year-over-year. The average VantageScore 4.0 credit score dropped by one point to 701 reflecting the decrease in creditworthiness for the average consumer.

Consumers in the highest VantageScore credit tiers are showing increased signs of credit stress on a year-over-year basis,” said Susan Fahy, EVP and Chief Digital Officer at VantageScore. “We’re also seeing a marked divergence in secured versus unsecured lending. Balances are increasing for auto loans and mortgages, while new credit originations are down. Sustained inflation for car and house prices is driving higher balances in these credit categories.

Watch CreditGauge LIVE for additional key insights from the July 2025 edition of CreditGauge that include:

AVERAGE VANTAGESCORE 4.0 DIPS TO 701: The average VantageScore 4.0 credit score slipped to 701 in July, down one point from June. VantageScore’s Subprime tier grew by 0.6 points from 18.1% to 18.7% between July 2023 and July 2025, swelling the ranks of consumers more likely to face repayment challenges. Conversely, the VantageScore Prime tier shrunk by 1.4% over the same period.

MORTGAGE, AUTO LOANS DELINQUENCIES AND BALANCES INCREASE: Mortgage and Auto Loan credit delinquencies saw the largest year-over-year uptick in the early-stage category (30-59 DPD), up 0.11 and 0.05 points, respectively. Auto Loan and Mortgage balances also increased on a month-over-month basis, while originations decreased for Auto Loans and held steady for Mortgages.

SECURED ORIGINATIONS SOFTEN: Auto Loan originations fell to 1.42% in July 2025 after peaking at 1.76% in April. Mortgage originations were relatively flat from June to July 2025 but stood 0.04% higher than in July 2024. These softening trends in originations are likely due to a combination of reduced demand and tighter lending standards.

Follow VantageScore on LinkedIn and YouTube to watch CreditGauge LIVE, a monthly video series featuring our latest insights on consumer credit data and analysis.

About VantageScore CreditGauge™

CreditGauge is provided both as a monthly analysis to industry stakeholders as well as through a series of interactive tools at VantageScore.com, which also includes Inclusion360®, RiskRatio™ and MarketGain™. Stakeholders can use the tools to execute additional queries on credit metrics and compare current levels to a pre-pandemic timeframe, starting with January 2020. CreditGauge solely represents the views and analysis of VantageScore and does not necessarily reflect or represent the views of the Nationwide Consumer Reporting Agencies (NCRAs) - Equifax, Experian, and TransUnion.

About VantageScore®

VantageScore is the fastest-growing credit scoring company in the U.S., and is known for the industry’s most innovative, predictive and inclusive credit score models. In 2024, usage of VantageScore increased by 55% to hit 42 billion credit scores. More than 3,700 institutions, including the top 10 U.S. banks, use VantageScore credit scores or digital tools to provide consumer credit products and generate greater insights into consumer behavior. The VantageScore 4.0 credit scoring model scores 33 million more people than traditional models. With the FHFA mandating the use of VantageScore 4.0 for Fannie Mae and Freddie Mac guaranteed mortgages, the company is also ushering in a new era for mortgage lending and helping to close the homeownership gap.

VantageScore is an independently managed joint venture company and owners include the three Nationwide Consumer Reporting Agencies (NCRAs) - Equifax, Experian, and TransUnion.