Let us know who you are

Inclusion360® Powered by VantageScore®

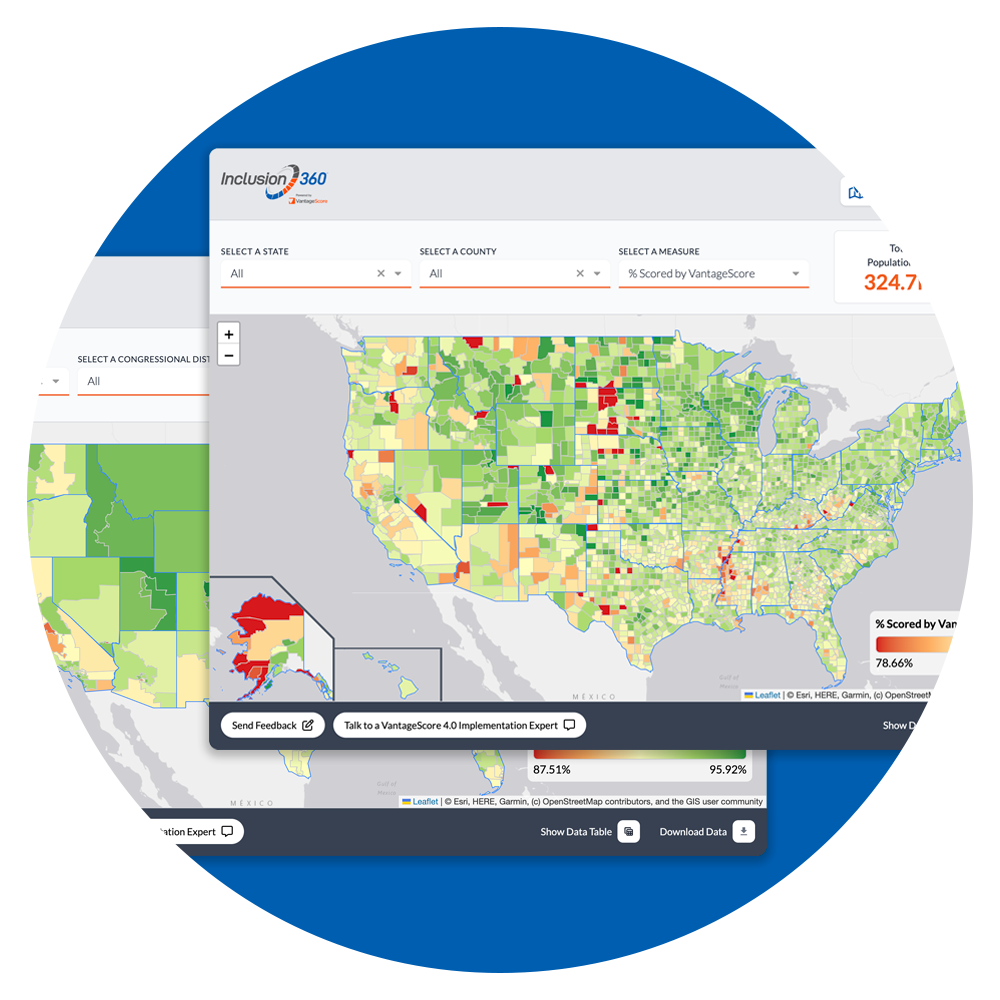

Pinpointing Opportunities for Financial Inclusion

What is Inclusion360®?

Financial inclusion and its impact on racial wealth equality remain one of the most important issues facing consumers, lenders and policy makers. To enable greater financial inclusion, VantageScore has launched Inclusion360. The groundbreaking, open access, and interactive analytics platform uses comprehensive data sets to uncover previously underserved consumers by geographic market. VantageScore is an industry leader in driving financially inclusive credit outcomes for traditionally underserved groups.

How to Use Inclusion360

Based on anonymized consumer credit data from Equifax, Experian and TransUnion and using the VantageScore 4.0 credit scoring model, there are approximately 33 million “newly scorable” consumers in the United States. “Newly Scorable” consumers are those who are not scorable using conventional credit scoring models but can be scored by VantageScore 4.0.

Assess the "newly scorable" opportunity in each type of consumer population segment and data points below:

Percent of conventionally scored

Proportion of credit-eligible consumers in selected area that are scored by conventional models, based on publicly available scoring criteria informationPercent of newly scored

Proportion of credit-eligible consumers in selected area that are newly scored by VantageScore 4.0Percent scored by VantageScore

Proportion of credit-eligible consumers in selected area that are scored by VantageScore 4.0. (Including conventionally and newly scored populations)Average VantageScore credit score

Average VantageScore 4.0 generated for credit-eligible consumers in selected areaPercent newly scored 620 and above

Proportion of consumers newly scored by VantageScore 4.0 in selected area where score generated in 620 and aboveNewly lendable opportunity

Estimated number of consumers newly scored by VantageScore 4.0 in selected areaGeographic Areas Available

NOTICE TO USERS: All data and information provided in and by Inclusion360 is for informational purposes only and should not be relied upon for financial, marketing, legal, technical, or other purpose or advice. Users are responsible for compliance with all applicable laws and regulations when using such data and information, including fair lending laws which require equitable treatment of all credit applicants without regard to prohibited factors such as race, color, or national origin. Consistent with VantageScore’s mission to be a leader in increasing financial inclusion and equitable access to mainstream credit, Inclusion360 identifies potential opportunities to use VantageScore credit scoring models to expand access to credit in underserved communities. It is unlawful for a lender to discriminate on a prohibited basis in any aspect of a credit transaction. Users should not under any circumstances use Inclusion360 to facilitate credit-related decisions using any prohibited discriminatory factor or the illegal practice of “redlining” (avoiding to provide services to individuals living in communities of color because of the race or national origin of the people who live in those communities), or for any other prohibited purpose.

Please review these Terms of Use before using or accessing Inclusion360. Inclusion360 is provided "as is" and on an "as-available" basis. VantageScore has no obligation to update any of the data and information provided in and by Inclusion360.

Depictions of VantageScore credit scores are not a guarantee of obtaining a VantageScore credit score or of obtaining a score in any credit score range depicted as lendable. VantageScore results may vary and not all lenders use VantageScore 4.0 or may use a different version of a VantageScore credit scoring model.

Inclusion360 uses the U.S. Census Bureau’s Congressional District Relationship files to map Congressional Districts to ZIP code data. The Congressional Relationship files are based on 2010 Census and the Congressional Districts of the 116th Congress (January 2019 - January 2021). Inclusion360 has not been updated to reflect the limited number of changes to Districts for the 117th Congress.

Geo-coding: A significant portion of the analysis used to generate the estimate of information and data provided in and by Inclusion360 is based on the geo-coding of consumer credit data using the U.S. Census Bureau and U.S. Department of Housing and Urban Development geo-coding sources. Inclusion360 maps zip-code level data to sub-geographies such as PUMA, CBSA, Congressional District and County.

The information and data provided in and by Inclusion360 (other than third-party information) and their arrangement, are copyright ©2025 by VantageScore, LLC. All rights reserved. Subject to the Terms of Use, Inclusion360 and the information contained herein may be used solely for personal, informational, and noncommercial purposes or, if you are a VantageScore-authorized entity, for internal business purposes. Except as otherwise provided, you may not modify, copy, distribute, transmit, post, display, perform, reproduce, publish, license, create derivative works from, transfer, or sell any pages, data, information, software, products, or services obtained from or through Inclusion360 unless you have obtained the prior written permission of VantageScore.

Sources: Geocoding Sources: Zip code to Census tract relationship file, Census tract to PUMA relationship file, Code Tabulation Area (ZCTA) Relationship File Record, Zip code CBSA file is used from the HUDUSER Office of Policy development and Research website, 2010 Congressional District Relationship Files (Nation-based).